How to Read Your Credit Report: A Beginner's Guide

Many people focus entirely on their overall 3 digit credit score when applying for offers. But this score is calculated from a credit report, which simply contains the raw data.

Your credit report serves like a financial resume, tracking how you’ve managed your debts, loans, and credit cards over time. Understanding how to read your credit report allows you to monitor your finances and protect yourself against identity theft.

It should be checked periodically to gain additional insights and to spot any reporting inaccuracies, which can damage a score.

Accessing Your Credit Report

Under Federal Law, you’re entitled to a free annual credit report from each of the three major bureaus (Experian, Equifax, TransUnion) once a year. The bureaus extended this to allow consumers to download a free report each week, but they can change this at their discretion.

You’re also entitled to additional reports in specific circumstances, including if you’re on public assistance, have received an adverse action notice, or suspect the report is inaccurate due to fraud or identity theft.

Reports can be accessed through the official Annual Credit Report website. You probably don’t need to monitor credit on a weekly basis, but monthly checks are definitely recommended. But you will need to check reports from all three bureaus, as not all lenders report to each bureau. This is a key point to bear in mind.

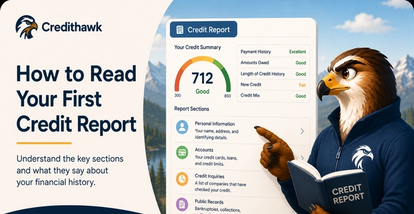

Remember that it typically takes six months to generate a FICO score and 30 days for a VantageScore. A score is not needed to access a credit report, however. When you do look at your credit report for the first time, it will be broken down into four major sections.

1. Personal Information

The first section of your credit report contains identifying details. This section is used by credit reporting agencies to verify your identity and ensure your accounts are not mixed up with someone else's. This section typically includes:

- Your full name (plus aliases or former names)

- Your Social Security number (which is usually partially masked for security)

- Your date of birth

- Your current and previous physical addresses

- Your employment history

While the information in this section does not directly impact your credit score, it should still be reviewed. An incorrect address, unfamiliar name variation, or typo in your Social Security number can indicate a clerical error (or early signs of identity theft).

2. Credit Accounts

This is the core of your credit report. It displays your credit history, listing your open and closed accounts one by one.

This section is generally divided into two categories: Satisfactory Accounts (accounts paid as agreed) and Adverse Accounts (accounts with late payments, charge-offs, or collection status). For each account, you’ll find the following details:

- The Creditor Name: The financial institution that issued the credit.

- Account Type: Whether the account is revolving (such as credit cards) or installment (such as auto loans, student loans, or mortgages).

- Credit Limit or Loan Amount: Your maximum spending limit or original loan size.

- Current Balance: The amount you currently owe.

- Payment History: A monthly grid showing whether you paid on time. Credit bureaus use specific codes to track this history, such as a check mark or "OK" for on-time payments, and numbers like "30," "60," or "90" to show how many days past due a payment was.

Negative information, such as missed payments, will typically remain on your credit report for seven years from the date of the first missed payment. Positive accounts closed in good standing can remain on your report for up to 10 years.

3. Collections and Public Records

If you fall severely behind on a debt, the original creditor may write off the debt as a loss and sell it to a third-party collection agency. When this happens, a Collection Account is added to your credit report. This section includes:

- The name of the collection agency

- The name of the original creditor

- The original debt amount and the current balance owed

- The date the collection account was opened

Additionally, this section of your report contains relevant Public Records gathered from state and federal court documents. Today, bankruptcies are the primary public record listed on consumer credit reports. Civil judgments and tax liens are no longer included in standard credit files.

4. Credit Inquiries

Whenever a business or individual requests to view your credit history, an inquiry is recorded on your credit report. There are two distinct types of inquiries:

- Hard Inquiries: These occur when you actively apply for credit, such as a credit card, auto loan, or mortgage. Hard inquiries are visible to potential lenders and can temporarily lower your credit score by a few points. They remain on your report for two years.

- Soft Inquiries: These occur when you check your own credit report, or when a company performs a background check for pre-approval offers or employment screening. Soft inquiries are only visible to you and have absolutely no impact on your credit score.

Reviewing and Disputing Credit Report Errors

It’s not uncommon for credit errors to show up on reports. But you’ll never spot them unless you regularly check, understand, and monitor your credit.

Remember, credit can affect your ability to qualify for credit cards, mortgages, auto-loans, insurance, and more. The bureaus are legally obligated to correct errors for free, so there’s no cost to file a dispute.

Each bureau has a distinct dispute process, conducted by phone, mail, or online. But you’ll need to be logged in to the portal first.

- File a credit dispute with Equifax.

- File a credit dispute with Experian.

- File a credit dispute with TransUnion.

The bureaus have thirty days to investigate disputes. For simple errors, such as a misspelled name or outdated balance, you can use the online form. But for more complicated errors such as a mixed file or incorrect bankruptcy listing, you may want to use certified mail to create a binding paper trail.

Why You Should Check Your Credit Report Regularly

Your credit report is the foundation of your credit score. By reviewing it regularly, correcting errors promptly, and understanding what lenders see, you'll be in a much stronger position when applying for future credit.

Aside from errors, it still helps to regularly read your report in order to understand your credit score in more depth. It’s a dynamic system with many moving parts, and it doesn’t stay still. By checking your report regularly, you can keep in touch with updates that may help you to build stronger credit over time.

Daniel O'Keeffe

Financial Copywriter

Financial Copywriter. Bachelor of Laws (University of Limerick) & Masters in Computer Science (University College Dublin). Worked as junior consultant in J.P. Morgan (New York), State Street (Boston), RBS (London). Now interested in personal finance and geo-arbitrage of different kinds.